Home insurance is evolving rapidly as connected technologies become embedded in everyday living. Traditional insurance models relied on static assessments and historical averages, often failing to reflect real-time risk. Today, smart home insurance is changing that equation by using connected devices to continuously assess household conditions and behaviors. By leveraging IoT risk data, insurers can better understand actual exposure, introduce dynamic pricing, and design more responsive policies. This shift is not only transforming how premiums are calculated but also encouraging safer homes and more transparent relationships between insurers and policyholders.

How Smart Home Insurance Uses Connected Devices

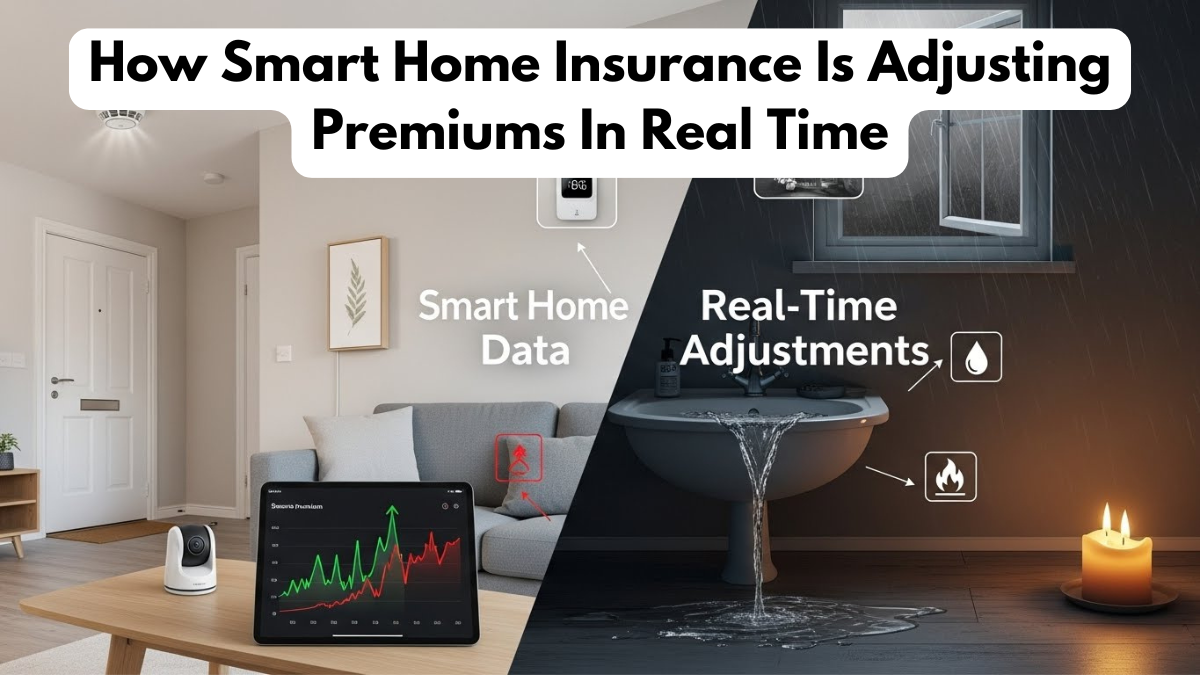

At the core of smart home insurance is the integration of connected sensors and devices throughout a property. Smart smoke detectors, water leak sensors, security cameras, and thermostats generate continuous IoT risk data that reflects real-time conditions. Instead of relying solely on location or construction type, insurers analyze live signals such as temperature fluctuations, moisture levels, and occupancy patterns. This data-driven approach allows policies to be tailored to actual behavior and maintenance practices. As a result, dynamic pricing becomes possible, rewarding homeowners who actively reduce risk through proactive monitoring and timely interventions.

Real-Time Risk Assessment and Dynamic Pricing

One of the most significant innovations in smart home insurance is the move toward real-time risk assessment. Continuous IoT risk data enables insurers to adjust premiums based on current conditions rather than annual reviews. For example, a home with functioning leak sensors and monitored alarms may qualify for lower rates through dynamic pricing. Conversely, unresolved hazards can trigger alerts that prompt corrective action. This responsiveness aligns premiums more closely with real risk and encourages policyholders to maintain safer environments. Over time, policies evolve from static contracts into adaptive agreements that reflect ongoing risk management.

Benefits for Insurers and Homeowners

The adoption of smart home insurance delivers advantages on both sides of the market. Insurers benefit from reduced claims frequency and improved loss prediction through accurate IoT risk data. Homeowners gain more control over costs and greater transparency into how premiums are determined via dynamic pricing. Key benefits include:

- Lower premiums for proactive risk reduction

- Faster claims handling supported by device data

- More personalized policies based on real behavior

- Improved home safety through continuous monitoring

These benefits demonstrate how connected insurance models align incentives between insurers and customers.

Comparing Traditional Insurance and Smart Home Insurance

A comparison helps illustrate the structural shift brought by smart home insurance.

| Aspect | Traditional Home Insurance | Smart Home Insurance |

|---|---|---|

| Risk assessment | Periodic and static | Continuous IoT risk data |

| Premium calculation | Fixed annual rates | Adaptive dynamic pricing |

| Policy flexibility | Standardized policies | Personalized and responsive |

| Claims prevention | Reactive | Proactive monitoring |

| Customer engagement | Limited | Ongoing and interactive |

This table highlights how smart models outperform traditional approaches in accuracy, fairness, and prevention.

Privacy, Data Use, and Policy Design

As smart home insurance expands, questions around data privacy and transparency are increasingly important. Insurers must clearly communicate how IoT risk data is collected, stored, and used within policies. Clear consent mechanisms and data protection standards are essential to maintain trust. When implemented responsibly, dynamic pricing can be seen as fair rather than intrusive, especially when customers understand how safer behavior leads to tangible savings. Thoughtful policy design ensures that technology enhances choice and control rather than creating confusion or concern.

Future Outlook for Smart Home Insurance

Looking ahead, smart home insurance is expected to become more sophisticated as device ecosystems mature. Advanced analytics will refine dynamic pricing models, while broader device compatibility will enrich IoT risk data streams. Insurers may introduce modular policies that adapt automatically as homes add or remove smart devices. As adoption grows, this approach could set new industry standards, shifting insurance from a reactive service to a continuous partnership focused on prevention, safety, and shared value.

Conclusion

The rise of smart home insurance marks a fundamental change in how risk is measured and managed. By harnessing real-time IoT risk data, enabling fair dynamic pricing, and designing adaptive policies, insurers and homeowners alike benefit from safer homes and more accurate premiums. This technology-driven approach aligns costs with behavior, rewards prevention, and builds transparency into insurance relationships. As smart homes become more common, smart insurance models are poised to redefine protection for the connected age.

FAQs

What is smart home insurance?

smart home insurance uses connected devices and IoT risk data to assess risk continuously and adjust coverage and pricing accordingly.

How does dynamic pricing work in home insurance?

Dynamic pricing adjusts premiums based on real-time risk signals, rewarding safer behavior and proactive maintenance.

Do smart devices lower insurance premiums?

Often yes, because reliable IoT risk data supports lower risk profiles within insurer policies.

Is my personal data safe with smart home insurance?

Reputable insurers use strict data protection standards and clearly define how data is used within policies.

Can traditional policies transition to smart home insurance?

Many insurers offer hybrid options, allowing existing policies to integrate smart devices and benefit from dynamic pricing.

Click here to know more.